How the Blockchain connects one of the world’s biggest economic forums

by Nate Charles

Unlike one’s parents, the world actually gets more hip and modern as it gets older. Every generation makes its own revolution, and every generation fantasizes over what the future has in store. Technology has played a crucial role in some of the recent and major societal developments, all the way from cars to cell phones. One area that went fairly unnoticed in the midst of this “Technological Renaissance” was currency. After all, what could replace money, and how could such a thing be done?

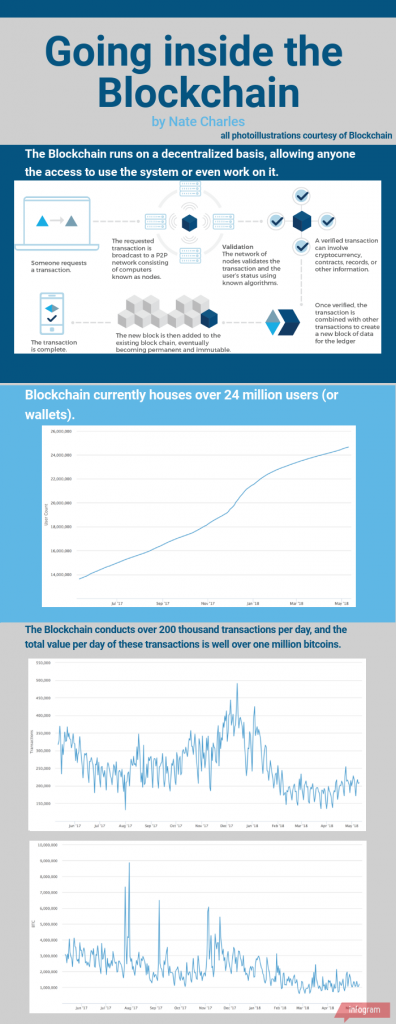

The words “bitcoin” and “cryptocurrency” have been floating around a lot recently, though for many, these are obscure topics that have little to no impact in their lives. In a recent Bark survey, only 13 percent of students said they had any holdings in the cryptocurrency market. However, Blockchain, the company behind these technologies, is much bigger than one might imagine. According to their website, Blockchain has over 24 million users, oversees 200 thousand daily transactions on their platform, operates in 140 countries and has raised over $70 million since the company was

founded in 2011. The company’s purpose, as stated through an email interview by communications lead Lulu Chang, is to “provide – to this day – the most frequently cited data on transactions, mined blocks in the bitcoin blockchain, charts on the bitcoin economy, and additional statistics and resources for developers.” For such a large and successful enterprise, it is relatively unknown, even though cryptocurrency itself has proved quite valuable in some instances. According to Statista, only eight percent of the total population of America owns any cryptocurrency and only 43 percent are aware that owning bitcoin is legal.

The Blockchain technology may seem daunting, as it controls the largest decentralized software platform for digital assets there

is, but it follows a simple chain of command: someone will request a transaction, whether it be a bitcoin transfer or a shipment, and that signal goes out to all administrators, called nodes. The nodes will work to verify the transaction – who and what it is – and then place it with other similar transactions into what is known as a block. That block gets added to a larger chain of other verified blocks, where all the transactions contained become final and secure. Then, the transaction is allowed to go through and the deal is done. Transactions can include anything from transferring bitcoins to another user to confirming digital movements of files, something many companies find very useful when dealing with logistics.

Though bitcoin and the Blockchain as a whole may seem complex and possibly useless, junior Noah Arias said he sees bitcoin as the future of economy due to its decentralized nature. Arias is a proud owner of $60 worth of bitcoin and self-proclaimed expert on both the Blockchain and cryptocurrency.

“I don’t think it’s going to replace everything like that, but there will be a steady increase into questioning ‘Hey, why don’t we have a currency that isn’t reliant on any government or bank to be a buffer in the system?’” Arias said.

Many people question how bitcoin and Blockchain are related. In sum, the technology is what runs the transfer of bitcoins (among other things), and the company is what runs the technology. The Blockchain technology processes thousands of bitcoin transactions every day, and the company’s app, ‘Block Explorer,’ is the leading bitcoin app on the market. In addition, it is also possible to obtain bitcoin while working on the Blockchain. Whenever a node confirms a transaction, they are paid a small stipend from the bitcoin marketplace for their work, a practice commonly referred to as “mining.” That’s not to say it’s easy money; in addition to spending extensive amounts of time verifying the buyer and seller as well as the item being transferred, nodes must go through a complex algorithm before the transaction can be placed in a block. In other words, mining is not for everyone, as one must spend hours first confirming the buyer, seller and product, then ‘cracking the code’ so-to-speak on a fancy numbers puzzle that allows the transaction to move along.

According to Chang, though bitcoin works just like any ‘normal’ currency (something that is exchanged for goods and services), its ability to optimize market functions such as monetary transportation, security and accessibility make it a very appealing choice.

“The digital asset, bitcoin, is used like other assets… [But] unlike traditional currencies, bitcoin is easily portable, divisible and

irreversible,” Chang said.

Arias listed many of the same aspects, adding that many are drawn to cryptocurrency as opposed to paper money because it alleviates some of the problems that surface in modern economics, the biggest one being the trust that one must allocate to others.

“I think the benefits you get are not having to deal with the cons of everyday currency,” Arias said. “It could be a new way of giving and receiving money without having to worry about the middleman, and that could [make it a lot easier] for people.”

Chang said Blockchain is striving to do just that; take out the intermediary. Chang also said that they hope to create a more “fair” financial future for economics.

“The Blockchain… allows users to transact directly, peer to peer, without a middleman to manage the exchange of funds,” Chang said. “Bitcoin increases system efficiency and enables the provision of financial services at a drastically lower cost, giving users more power and freedom.”

Arias said his biggest worry is that, due to a recent drop in value, many will see bitcoin and other cryptocurrencies as unstable and possibly lose interest. However, according to Arias, he firmly believes cryptocurrency is the next step in an economic revolution, one that will do away with paper money completely.

“I’m worried about the fact that people who saw that big dip are going to decide to lose interest or sell,” Arias said. “Cryptocurrency is a new interesting direction that could have a lot of good possibilities for the future. [It] could be the transfer from our normal everyday economics to… this unknown system of currency that’s better than ever before and bitcoin could be the bridge between the two.”

Blockchain is opening a new store in San Francisco, signalling that one of—if not the biggest—tech sectors in America is ready to go all-in on a trend that could change the way society deals with money forever. The company has doubled its workforce, and it will be merging with the startup Tsukemen to form a tech center in downtown. Though society still recognizes dollar bills as the preeminent currency in this country, people are beginning to recognize that bitcoin is not just another internet fad; it might just be the future of the economy.